Introduction

Data and Methods

Material

Conceptual structure and Methodology

Participation of smallholder farmers in Saving and Credit Cooperatives

Impact of SACCO on income of smallholder farmers

Bi-direction relationship of Income and participation in SACCO

Result and Discussion

Descriptive statistics of smallholder farmers

Factors limits the participation of smallholder farmers in SACCOs

Descriptive statistics on attractiveness to SACCO’s products/services to participants

Statistics of model variables and definition of variables surveyed May-July 2019

Factors influence the participation of smallholder farmers in Saving and credit cooperatives.

The factors affect the income of smallholder farmers in Rwanda

Determination of bi-directional relationship between MSACCO and income

Conclusion and Recommendation

Introduction

For past decades different studies revealed that access to finance is the shortest way to development of any country and whole world concern about ending poverty by opening up easy accessibility to finance for household, so poverty rate went on decreasing since past two decades (Rewilak, 2017). The promise of Saving and Credit cooperative is ability to reach out the poor household in both mobilizing and finance accessibility to them. SACCOs are playing big role in most of developing country in helping their members to increase income (Anania et al., 2015). and it is believed that microfinance enabled smallholder farmers to easily access to credit facilities without big collateral (Girabi et al., 2013). Saving and Credit Cooperatives (SACCOs) movement started in 2010 in different parts of Africa by establishing the law regulates these Microfinances. Some scholars confirmed that Saving and Credit cooperatives has been a good strategy for poverty reduction in some countries in Africa, according to the study done in Tanzania shows that Saving and Credit cooperatives is key among the factors for poverty reduction reduction (Kihwele et al., 2015).

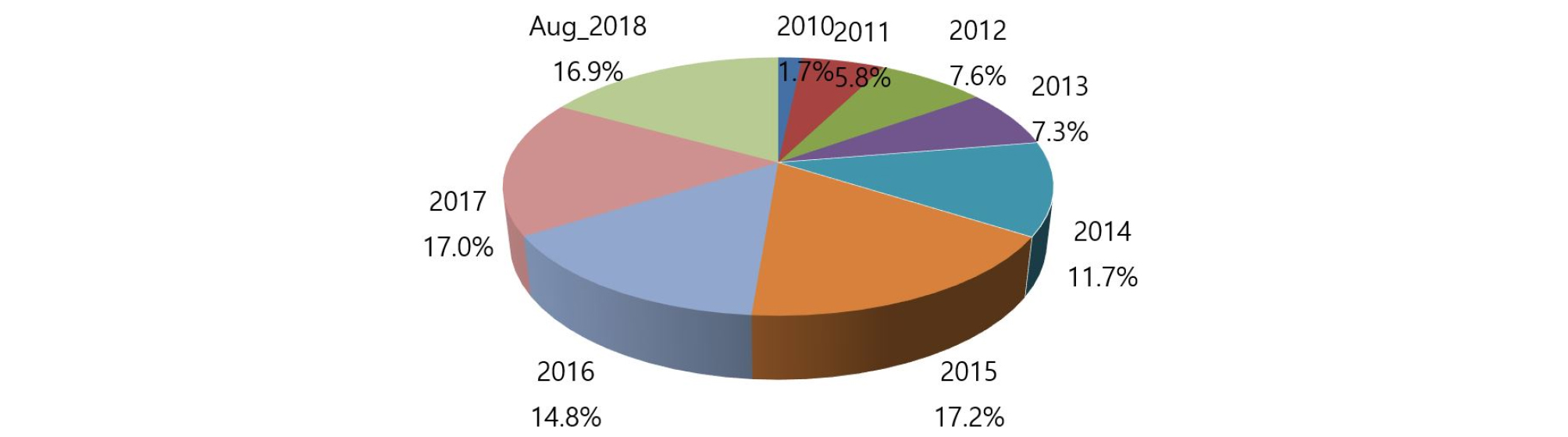

In Rwanda, Saving and Credit Cooperatives (SACCOs) are main provider of finance to smallholder farmers in rural areas (Nair et al., 2018). As at December 2016, out of the 472 microfinance institutions operating in Rwanda, 17 are microfinance institutions with limited liability company status; 455 are Savings and Credits Cooperatives (SACCOs): These include 416 Umurenge Saving and Credit Cooperative (U-SACCO) and 39 non U-SACCOs (Bank et al., 2017). The concept of Umurenge Savings and Credit Cooperatives (U-SACCOs) was based on an understanding that banks and other financial institutions were more concentrated in urban areas whilst the majority of the Rwandan population lives in rural areas and totally excluded from the formal financial institutions. Umurenge SACCOs are Sector level based Saving and Credit Cooperatives (one SACCO per sector level) and were established in 2008 with the aim to boost up rural savings and provide Rwandans with loans to improve their earnings and enhance their livelihoods. This program has contributed financial service in Rwanda, The Fig. 1.demonstrates percentage savings of members in U-SACCO each year, since 2010 to August 2018. Deposits of members in Saving and Credit cooperatives (SACCO) is over 67.3 billion Rwandan francs where 95% of this deposit was saved in U-SACCOs and 5% in other SACCOs.

U-SACCO program is an example of how financial inclusion can succeed when all stakeholders in a country pursue a special goal under a shared vision. Vision 2020 and the Financial Sector Development Program set out a vision of enhancing access to affordable financial services and establishing financial institutions in Rwanda. However, smallholder farmers are still facing challenge of boosting income generation as the recent study examined the economic lives with case studies from different continent of the world and it was found out that, poverty among small farmers is increasing and in most countries much higher than the national proportional of population exist below the poverty line (Rapsomanikis, 2015). The researcher pointed out facts backing up the statement, like in Plurinational State of Bolivia, national poverty is estimated to 61 percent and up to 83 percent of poor are from smallholders farmers are poor compared with a national poverty (Rapsomanikis, 2015). In Ethiopia, where 30 percent of the entire population lives under the national poverty level, the proportion of a population that exists below the poverty line is 48 percent are of smallholder farmers (Rapsomanikis, 2015). In Viet Nam, more than half of the smallholders are poor when in the country as a whole about 20 percent of the population lives in poverty and this paper went on insist on productivity of smallholder, which is currently increasing at decreasing rate (Rapsomanikis, 2015). Smallholder farming also is still facing challenge of income generation as large percentage of farming in Rwanda engaging in traditional way of farming, relying almost exclusively on manure for fertilizing the soil and on small land handed use of farming (hoes and machetes) for most agricultural activities (Verpoorten, 2014). UN stainable development strategies are to end poverty of every form and everywhere but among smallholder farmers is still big challenge for poverty reduction. Empirical on study done in Tanzania has proved that access to finance in rural areas leads to poverty reduction, the income of active members of SACCO is expected to increase from credit invested for high production for smallholder farmers who participated in SACCOs (Kwai and Urassa, 2015). Household’s income of smallholder farmers with access to credit is significantly higher than comparing households without access to credit (Muyombano et al., 2016). Impact of SACCOs on household has attracted different researchers, however the basing on reviewed studies, were limited at impact on household’s income at large but this articles more specific on smallholder farmers in Rwanda. Conducted the research on the U-SACCO as a tool for financial inclusion by using of descriptive and multiple regression analysis, it was revealed that there is a relationship between financial literacy and holding extra money in the pocket after joining SACCOs and the study show 63% SACCO leaders agreed there is relationship in engaging in SACCO and increase of income (Bosire et al, 2015). However, this study collected data from leaders of SACCO from 7 members of board of directors and 3 members of supervisory committee which show some biasness in study. Management team of SACCO can easily agree to give similar information than ordinary member. This study is an added knowledge to Previous research on income generation of smallholder farmers with respect to SDGs goal of ending poverty of all forms by 2030 (GA, 2015). Ending poverty among smallholders is still long journey for many developing countries and to reach out this go, countries may have to put different strategies for farmers to access to finance and this was inspiration for this study to come up with the main objective of this study is to assess the impact of saving and Credit cooperatives on income of smallholder farmers in Rwanda and this study is different from previous study in three ways. This study is more specific on impact of SACCOs on smallholders where others took interest in broad study impact of SACCOs on household in general and also, the study estimated factors affecting participation or not participation of smallholder farmers in SACCOs. Finally, the study discovered the bi-direction relationship between income and participation in SACCOs of smallholder farmers.

Data and Methods

Material

The study adopted a cross-sectional design and data were collected at a single point in time. This design was preferred, for despite its simplicity, it allows one to collect data about past and current experiences to identify possible associations (Kwai and Urassa, 2015). This study was conducted in BUSASAMANA Sector, Nyanza district, southern province of Rwanda between May and July 2019, Busasamana Sector in Located in Nyanza District in southern province of Rwanda. Geographically has area of 49.3 km2 and population of 42,870. The big part of this sector is rural area and main economic activities in this sector are substance agriculture and trading, most farming is done on small scale and main agriculture produce are rice, maize, beans, banana plant, peas, vegetables, Mushroom and coffee on small scale. The study used a cross sectional survey design where the purposive sampling was used to select 200 smallholder farmers where 124 are members of SACCO and 76 are non-members. The survey conducted by a numerator and questionnaires were designed for face-to-face interview. The data was analyzed by using Stata14 statistical software. Sample size is appropriate if it enables the researcher to make an unequivocal judgment that a statistical result is correct to a specified meaningful effect (Malone et al, 2016). This study used 200 sample sizes which was calculated and Since the proportion of the population was not known, the study assumed P=0.9, (1-P) = 1-0.9= 0.1, Z = 1.96 and d is assumed to 0.05. The results came out as 138.3 but the researcher used 200 sample size to have more accurate results, according to the study, the larger the sample, the smaller the margin of uncertainty (confidence interval) around the results (Conroy, 2020).

Conceptual structure and Methodology

This study used three models in responding to the objectives of the study. Linear regression Model was used to determine the effect of SACCO on income of small holder farmers, Logistic model to examine the factors that influences smallholder farmers’ participation in SACCO (Damodar, 2004). Seemingly unrelated regression (SUR) to analyses bidirectional relationship of participation in SACCO and income. Nine variables were used to in each empirical model to achieve the objective of this study. This study used three (3) econometric models in order to empirically achieve the objectives and 8 independent variables1) were employed.

1) Independent variables: X1=Age of participant, X2=Sex, X3=marital status, X4=Household size, X5=Education level, X6=Income source, X7=Requirements to join SACCOs, X8=Income.

Participation of smallholder farmers in Saving and Credit Cooperatives

The choice to participate in SACCO or not participate in SACCO can affect income of smallholder farmers. This ends up as bi-outcome dependent variables, dependent variables (MSACCO) is participation of smallholder farmers has two (2) outcome, probabilities of smallholder farmers to be a member and probabilities of smallholders farmers to be non-member of Saving and Credit cooperative (SACCO) and those variables are code as binary 1(one) for member and 0 (Zero) as non-member of Saving and Credit Cooperative. Logistic regression analysis model for dichotomous outcomes showed how the logistic regression is more important than other linear regression more when outcome are binary because mathematically is extremely flexible and easily used function and it has theoretical meaningful interpretation (Afolami et al., 2015). This study used logistic regression model to examine the participation decision of smallholder farmers in Saving and Credit Cooperative.

Binary logistic regression model does not make assumption about the distribution of the independent variables (Afolami et al., 2015). The relationship between the predictor and response variables is not a linear function in logistic regression; instead, the logistic regression function is used, which is the logit transformation of p:

| $$L=Log\left[\frac{P(x)}{1-P(x)}\right]=\beta_0+\beta_1X_1+\beta_2X_2+\cdots\;+\beta_nX_n$$ | (1) |

L stands for logistic model, P(x) is a probability of event to occur, is given by (1), then the probability of not event occur is 1-P(x) and then P(x) / (1-P(x)) is simply the odds ratio in favor of event to occur. And notations of is intercept regression is , and, are coefficient of independent variables and X1, >X2…Xn are independent variables of regression. The ratio of the likelihood of occurrence of an event to the probability of non-occurrence of the event as well the outcome of logit model and Since logistic regression calculates the probability of success over the probability of failure, the results of the analysis are in the form of odds ratio. Logistic regression also provides knowledge of the relationships and strengths among the variables. This Logistic formula can be used to estimate the change in probability of smallholder farmers who participated in Saving and Credit Cooperative (SACCO) and comparison with non- participation in SACCO provides the measurement the impact to smallholder farmers at end. Decision of smallholder farmer to participate in SACCOs (being a member of SACCO) is assumed to help them to earn more income and the below equation declares the variables employed.

| $$MSACCO(0,1)=\beta_0+\beta_1age+\beta_2sex+\beta_3MRTSTATUS+\beta_4HSHDSIDE\\\;\;\;\;\;\;\;\;\;\;\;\;\;\;\;\;\;\;\;\;+\beta_5EDUCLEVEL+\beta_6incomesorc+\beta_7RQMTS+\beta_8income+\epsilon$$ | (2) |

Impact of SACCO on income of smallholder farmers

This study also used linear regression model (OLS) to analyze the effect of the saving and Credit Cooperative in on income. Ordinary least-squares (OLS) regression is a generalized linear modeling technique that may be used to model a single response variable (dependent variable) and may be applied to single and well as multiple explanatory variables and also categorical explanatory variables that have been appropriately coded, this study adopted this model on analysis of impact of SACCO on income as single response dependent variable with multiple independent variables (Hutcheson, 2011). This model assumes there is linear relationship between independent variable and dependent variables (Hutcheson, 2011). Ordinary least squares model is written as below

| $$Y=\beta_0+\beta_1X_{1J}+\beta_2X_{2J}+\cdots\;+\beta_KX_{KJ}+\epsilon$$ | (3) |

The parameters βj, j=0, 1, 2……k are known as regression coefficients. This model describes a hyperplane in the k – dimensional space of the independent variables Xj’s. The parameter βj represents the expected change in the dependent variable Y which is income in this study per unit change in Xj , when all of the remaining predicted variables are constant. This study adopts this model to estimate the change of dependent variable Y (income) caused the change in participation in SACCOs as independent variable holding other variable constant.

| $$INCOME=\beta_0+\beta_1age+\beta_2sex+\beta_3MRTSTATUS+\beta_4HSHDSIZE\\\;\;\;\;\;\;\;\;\;\;\;\;\;\;\;\;\;\;\;\;+\beta_5EDUCLEVE+\beta_6INCOMESORC+\beta_7RQMTS+\beta_8MSACCO+\epsilon$$ | (4) |

Bi-direction relationship of Income and participation in SACCO

This study used SUR model find out bi-directional relationship of income and participation in (MSACCO) variables as this study assumed two variables are independent to each other. Simultaneously modeling of seemingly unrelated model is appropriate estimated two equations (Mujuru et al., 2020). Two variables are examined, Participation in SACCO and income are expected to have a bi-directional relationship and hence the need to estimate the two equations and the SUR model is supposed to presented as following (Zellner, 1962). We consider here a model comprising of M multiple regression equations of the form

| $$y_{ir}=\beta_iX_i+\epsilon_{ir},\;\;\;i=1,2,\;\dots,M$$ | (5) |

Here i represents the equation number, r=1,..,R is the time period. The number of observations R is assumed to be large, so that in the analysis we take R→∞, whereas the number of equations M remains fixed.

Each equation i has a single response variable y_(ir) and a k_(i)- dimensional vector of regressors X_(ir). If we stack observations corresponding to the ith equation into R -dimensional vectors and matrices, then the model can be written in vector form as

Where yiand are (R × 1) vectors, Xi is a (R × ki) matrix, and is a ki × 1 vector.

Finally, if we stack these m vector equations on top of each other, the system will take the form

The assumption of the model is that error terms are independent across time, but may have cross-equation contemporaneous correlations. Thus we assume that

| $$E\lbrack\epsilon_{ir}\;\;\;\epsilon_{is}\;\;\;\left|X\right.\rbrack=0$$ | (7) |

Basing on equation (5) this study M is considered to be 2(M=2), where Y1 Participation in SACCOs (MSACCO), Y2 is income of respondents (smallholder farmers) and X1 → X8 are explanatory variables for each equation. This model was used to analyze simultaneous effects of income and membership (Participation in saving and credit cooperative) more specific to check the bi-directional relationship for both income and participation in SACCO (MSACCO). SUR was capable in dealing with the correlation of error term between in Income and MSACCO among two multiple regressions.

This study has variables, which affect both regressors (Income and MSACCO) and also regressors (Income and MSACCO) are allowed to be endogenous variables to each other and previous study used SUR model to investigate bidirectional relationship between export and growth of developing countries (Kónya, 2006). This study generalized the two multiple equation into simultaneous equations model SUR, assuming there is correlation in both variable influence each other. Some identified factors used in estimating Income are Age, Sex, Marital status, Household size, education level, require to participate in SACCOs (RQMTS) and MSACCO. While MSACCO are Age, Sex, Marital status, Household size, education level, RQMTS (Requirement to participate in SACCO), Income source, and Income. A Seemingly Unrelated Regression Model comprises several individual relationships that are linked by the fact that their disturbances are correlated of which researcher assumed the correction of disturbance as mentioned above, in this study the simultaneity effect was acknowledged between Income and MSACCO (participation in SACCO) which were recognized as Endogenous variables.

Result and Discussion

Descriptive statistics of smallholder farmers

Table 1 presents the descriptive statistics of variables which describes main variables about smallholder farmers surveyed in Busasamana sector in south province of Rwanda in 2019. Among sample size of 200 of smallholder farmers, analysis demonstrates that 124 smallholder farmers of participated in SACCOs and 76 smallholder farmers are non-participants, most frequent gender of smallholder farmers participated in SACCOs is female (n=109, 54%) in this survey. Majority of smallholder farmers are aged between 22 and 40 years old (n=117,58.5%), and majority of smallholder farmers are married (n=174, 87%). Of total sample size, the most frequent smallholder farmers’ household size is made up of between one person to five people (n= 114,57%). The study revealed that most of Rwandans who engage in smallholder farming are of primary level education with most frequent in this survey (n=137, 68.5%) and primarily income source is from agricultural production with most frequent of n=178( 89%)of smallholder farmer surveyed as well most frequent grouped income earning is less than or equal to 20000 Rwandan francs per month(n=138, 69%), it was also revealed that most of farmers know(aware) about requirements to participate2) in SACCOs with most frequent in this survey (n= 163, 81.5%) of which demonstrate 18.5% farmers may be limited to participate in SACCOs because they don’t know about requirements.

2) The requirements to participate in SACCOs are 1) paying membership fee, 2) attending the meeting, 3) paying monthly fee, and 4) meeting quantity of output.

Table 1.

Descriptive statistics of sampled smallholder farmers in Rwanda

Factors limits the participation of smallholder farmers in SACCOs

The results from Table 2,demonstrates that majority of smallholder farmers who doesn’t participate in saving and credit cooperative (SACCO) because of distance from smallholder farmer’s house to the SACCO which counts (N=87, 43.5%) which followed by second highest frequency of smallholder farmers claimed of not participated because of lack of information on products/ services of SACCO (N=41, 20.5 %), this study also revealed that smallholder farmers do not participate in SACCO because SACCOs in Rwanda are non- automated in terms of transactions (N=34, 17%), and least smallholder farmers found out that did participate in SACCO due high membership fee, small loan issued by SACCO and due high interest rate with least frequency of N=18 (9%), N=8 (4%) and N=3 (1.5%) respectively.

Table 2.

Statistics on limitation on participants in SACCOs

| Reasons not join | Frequency(N) | Percentage% |

| Non automated | 34 | 17.0 |

| Distance | 87 | 43.5 |

| Small loan | 8 | 4.0 |

| No information | 41 | 20.5 |

| High interest rate | 3 | 1.5 |

| High membership fee | 18 | 9.0 |

Descriptive statistics on attractiveness to SACCO’s products/services to participants

The results in Table 3 demonstrate statistics 12.5% of smallholder farmers received loan from SACCO and 87.5 % didn’t receive loan and concern the use of accounts, majority of participants in hold current accounts which count of 73 % of member of SACCO and 27 % of participant hold long-term/saving account.

Table 3.

Statistics on attractiveness of products provided to participants by SACCOs

| Service provided | Frequency | Percentage |

| Received loan | 25 | 12.5 |

| Not received loan | 175 | 87.5 |

| Current account user | 146 | 73.0 |

| long-term account user | 54 | 27.0 |

Statistics of model variables and definition of variables surveyed May-July 2019

Variables provided in the Table 4 are summary statistics of variables used in analysis; nine variables (9), 200 observations for each variable were sampled. According to survey average of 0.62 smallholder farmers participated in SACCO (MSACCO); highest number of smallholder farmers are female with average 0.545 and most of them are married with average 0.87 married farmers; average income of smallholder farmer in Busasamana sector is 22725 FRW, higher earned 195000 and lowest earn 10000 FRW and main income source for most farmers is farmer production with average 0f 0.89. Average education level of smallholder approximate 7 years (primary level with first year of secondary level), smallholder with highest level is 18 years which equivalent to Master’s degree and lowest education level is 0 (un school) farmers; average age of smallholder farmers approximately 41 year old, youngest is 22 year old and oldest is 84 years old and size of highest household size of this sample is consist of 11 people and lowest size is made of one person with average size 5 person per household. This survey also demonstrate the average smallholders know about requirements to participate (RQMTS) in SACCO to 0.815.

Table 4.

Summary statistics of model variables surveyed between May-July 2019

Factors influence the participation of smallholder farmers in Saving and credit cooperatives.

From data analysis in response to second of objective of this study, logistic regression model was used and the outputs are shown in the Table 5 revealed the results on factors influence the participation of smallholder farmers in Saving and credit cooperative (SACCO). The findings show variables EDUCLEVEL (education level), RQMTS (requirements) and income are all significant variables at p < 0.05, p < 0.01, p < 0.001. The interpretations of the results are following:

Table 5.

Results of logistic model on factors that influence smallholder farmer participation in SACCOs

Coefficient of Education level of smallholder farmers is significant at p < 0.01 and has negative influence on decision taken by smallholder farmer to participate in SACCO. This implies that smallholder farmers acquire higher education level, the likelihood of participating in SACCO tend to decreases. This is because, this study is limited to smallholder farmers , according to recent study revealed, majority of people in agriculture activities did not acquire formal education because those who obtain knowledge (education) participate less in rural agricultural activities since they look for other opportunities out of farming, this ends to less educated people in farming and this is the main reason to which this study shows that high educated farmers are less likely to be a member of SACCO. This study focused only on smallholder farmers and since it is specific on smallholder farmers, it clearly indicates that as high education is acquired less participation in Saving and credit cooperative (SACCO).

The results found out that coefficient of requirement to join SACCO (RQMTS)is positive and strongly significant influence smallholder farmers on being the member of SACCO. The positive outcome implies as more requirements put in place to join saving and credit cooperative there is like hood of farmers to participate in SACCOs. This point out that more requirements more participation in SACCOs, this because people put their money in financial institution where they trust requirements.

The results on coefficient of Income revealed that income at p < 0.05 is strongly positive and significant influence smallholder farmers to participate in SACCO. This positive result means, for smallholder farmers who earn more income are more likely to participate in SACCO, because they are looking for security of their net income as well as to benefit from savings. This result is backed up by other previous study which examined the determinants of participation of household in SACCO in Uganda, their results indicated that the likelihood of membership in SACCOs and depositing in a SACCO increased with growth in incomes of household (Mpiira et al., 2013). It implies that earning income affect the decision taken by smallholder farmers to be member or not member in positive association.

The factors affect the income of smallholder farmers in Rwanda

The findings out of 200 observations reveals that 5 variables (Household size, Education level, requirement, MSACCO, income source) are all significant at *p < 0.05, **p < 0.01, ***p < 0.001. The interpretations below for predictor variables provide information on associated dependent variable (income) based on outcome shown in Table 6. Household size for smallholder farmer is statistically significant at p < 0.01 and positively influence on income of smallholder farmers. The positive relationship means increase household size smallholder leads to large number of labor for farming which results in high production and hence increase of income of household. The outcome of this study shows importance of household size in income generation strategies of smallholder farmers. This result is in line with outcome previous which confirmed that annual income is positive and significant associated number of household (Ngongi et al., 2014).

Table 6.

Results of ordinary least squares on factors affecting smallholder farmers' income

Coefficient of education level is positive and significant at p < 0.001 influences on income of smallholder farmer in Rwanda. The positive output of education level demonstrates that smallholder farmers who acquire more education level access on more information on farming technics and which help them to increase productivity as well as access to market for income increment. This indicates the importance of education of smallholder farmers for income generation, which result in acquired knowledge in agricultural production and market access.

Coefficient of RQMTS (requirement to join SACCO) is negative and significant at p < 0.05 influences on current income. Negative coefficient indicates that more requirements put in place to join SACCO tends to decrease the current net income of participants, because for more requirements requires more money to pay which decrease current net income (take home income).

MSACCO (membership of SACCO) is significant at 5% and strongly positive influence on income. The positive influence implies that smallholder farmers who are members of Saving and credit Cooperatives (SACCO) tend to have higher income than non-members. Smallholder farmers who are members of SACCO access to finance easily and invest in farming technology for high production as well as help in accessing to market for their productivity to direction of more income generation.

Income source Coefficient is negative and significant at p < 0.001 influencing on income. This indicates with fact that smallholder farmers with more income source tends to have less net income. This study is backed up by previous study, according to relationship between non-farm income and overall income is U-shape because for long-term investments and barriers to enter into market which tends to decrease overall income of farmer. This demonstrates importance of smallholder farming giving more time and high technology in farm production can generate more income.

Determination of bi-directional relationship between MSACCO and income

Seemingly unrelated regression model (SUR) was used to examine whether participate in saving and credit cooperative (SACCO) and income influence each other. This model assumes that both income and MSACC are Endogenous variables. All the rest of variables are exogenous and are same for both equations. Variables used are Age, sex, marital status, household size, education level, requirements, income, income source, MSACCO. The outcomes of seemingly unrelated regression are shown below:

In Table 7 shows correlation between two estimates equation was tested by Breusch-Pagan test of independence and is significant because P is very small (p=0.020) which implies there is correlation between across two equations.

Table 7.

Results of SUR model on determination of bi-directional relationship between MSACCO and income

Coefficients of both MSACCO and Income are significant at p < 0.001 and strongly positive influence each other. This implies that smallholder who earner more income tends to participate in Saving and Credit Cooperatives (SACCO) and as well as smallholder farmers who participate in SACCO earn more income than non-members.

Coefficient of number of household of smallholder farmers is negative influence and significant at p<0.05 to MSACCO, negative sign implies increase smallholder farmers with higher number of household tend to less likely participate in SACCO, the results with Logistic is household size is not significant, where as in SUR model household size is significant. Coefficient of household size to income is positive and significant at p < 0.01 to income which implies that smallholder with bigger number of household tend to have higher income which means more household number may have high income earning since individual member contribute to income on household.

Education level of smallholder of farmer has negative influence to MSACCO and significant at p < 0.001, this indicates that for more educated smallholder tends to less participate in SACCO, this is due to more educated people tend to migrate from rural areas which means most of smallholder farmers are less educated. In contrast, Coefficient of Education level of smallholder has positive influence on income and significant at p < 0.001, positive sign implies that more educated smallholder farmers tends to earn more income, because more educated people always access to information where to invest and earn more. The results of education level variable from SUR Model are better than running regression individually; coefficients are bigger in SUR model results compared to individual equation.

Coefficient of requirements to join SACCO (RQMTS) to MSACCO is positive influenced and significant at p < 0.001. This positive sign means as more requirements put in place to participate in SACCO, smallholder farmers tend to participate in SACCO. This explained by the fact that most people put trust/money more where they can have many agreements/contract with financial institution, for any financial requirement is followed with certain contract. However, Coefficient of requirements to join SACCO (RQMTS) to income is negative influenced and significant at p < 0.001. This implies as more requirements put in place net income of smallholder farmers decrease, since requirement cost more that why more requirement less net income.

Income source Coefficient is negative and significant at p < 0.001 influencing on income. This indicates with fact that smallholder farmers with more income source tends to have less net income. This study is backed up by previous study, relationship between non-farm income and overall income is U-shape because for long-term investments and barriers to enter into market which tends to decrease overall income of farmer. This demonstrates importance of smallholder farming giving more time and high technology in farm production can generate more income (Rapsomanikis, 2015).

Conclusion and Recommendation

This paper is purposely to assess the impact of SACCO on income of smallholder farmers. Primary data was collected and analyzed with help of 3 models, both OLS and SUR results demonstrated the impact of SACCO on income but OLS results may have biasness because of endogeneity between MSACCO (participation in SACCO) and income. The study also revealed that standard errors of SUR estimator are lowest and highest precision of estimate compared to OLS. SUR estimates are consistent compared to OLS estimates because SUR takes in account the correction in error terms. (Cadavez and Henningsen, 2012). Basing on the results from SUR estimator, This study found that participation in Saving and credit cooperatives (SACCO) has impact on income of smallholder farmers in Rwanda, there is increasing in income earning of members than non-members of SACCOs and the finding of this study is backed up by previous studies revealed the impact of Saving and credit cooperative on economic development and wellbeing of members/ households in Rwanda but those studies remained limited at well-being household in general. In addition the study found out that females are mostly engage in smallholder farming. Furthermore, findings of this study also revealed that income of smallholder farmers are significantly explained by other factors such as education level of smallholder farmers and most of farmers are primary level educative, Requirements put in place to Join SACCO, household size of smallholders of which most farmers are aware of requirement to participate in SACCO and also income source of it was found (Jonathan and Marthe, 2018).

Study tacked on factors influence decision of smallholder farmers to participate in Saving and credit cooperative (SACCOs) and results found that factors such as Education level, income and Requirements put in place to Join SACCO to be significantly affecting the decision taken by smallholder farmers to engage in SACCOs.

The finding also demonstrates that there is bi-direction effect between Income and participation in saving and credit cooperative (SACCO), smallholder farmers who earn more participates in SACCOs for security of their money and as well as participation in saving and credit cooperative boost income earning due to investment done out of loan and interest from savings. The study also tacked how members of SACCO grabs the services provided, it was found that it is small percentage of smallholder farmers request for loans, only 12.5% received loan and most of smallholder farmers hold current account compared to saving/long-term account holders which counts 73 percent and 27 percent respectively. However, the findings of this study disclosed the factors hinders smallholder farmers to participate in Saving and Credit cooperative, main factors revealed are two, long distance from SACCO to resident of some smallholder farmers and lack of information on some smallholder farmers on saving and credit cooperative’ operations. For previous studies urged that contributed much to accessibility finance in Rwanda of which every Umurenge SACCO is located in 5 KM radius to Rwandan population. However, this study revealed that 43.5% of non-members claimed of long distance from their resident, which implies some smallholder farmers whom are not located in 5KM radius. Finally, this study came up with following recommendations.

Government should motivate more farmers to participate in SACCOs, this study found out that members of SACCOs earn more than non-members since income generation for smallholder farmers. Motivating by put incentives to join can boost income generation of farmers as well economy of the country as it should be shortest way to end poverty in all corners of the country.

Government should create off farm activity for smallholder farmers for added income earning since this study found that there is bi-direction relationship in participation in SACCO with income of smallholder farmers which with can lead to increase financial inclusion as well as more income generation which may result from interest gained for long-term savings.

Both Rwanda cooperative Agency and National Bank of Rwanda as regulators of SACCOs should access SACCOs located far from smallholder farmers and establish more branches for ease of accessibility to SACCO.

Government should put effort in automating SACCOs to attract more members to participate and for easy access to the product/service of SACCOs where ever in Rwanda.